Unmasking Financial Errors: An Ensemble Approach to Anomaly Detection in Investment Banking

In the complex and fast-paced world of investment banking, the accuracy of risk calculation systems is paramount. A new research paper introduces a groundbreaking methodology, the Ensemble Quality Assessment Framework (EQAF), designed to detect anomalies in risk valuation outputs. This innovative approach leverages a combination of statistical and machine-learning methods to enhance the reliability of financial models and, ultimately, safeguard the integrity of the financial system.

Understanding the Problem: Risks of Undetected Anomalies

The research underscores a significant concern: errors in risk valuation, often stemming from data-feed failures, misconfigured models, or system malfunctions, can lead to substantial financial losses. Historical instances, such as the infamous "London Whale" incident at JPMorgan Chase, illustrate how unnoticed anomalies can culminate in billion-dollar losses. These incidents highlight the urgent need for robust mechanisms to detect potential errors before they disrupt financial operations.

Introducing EQAF: A Novel Framework

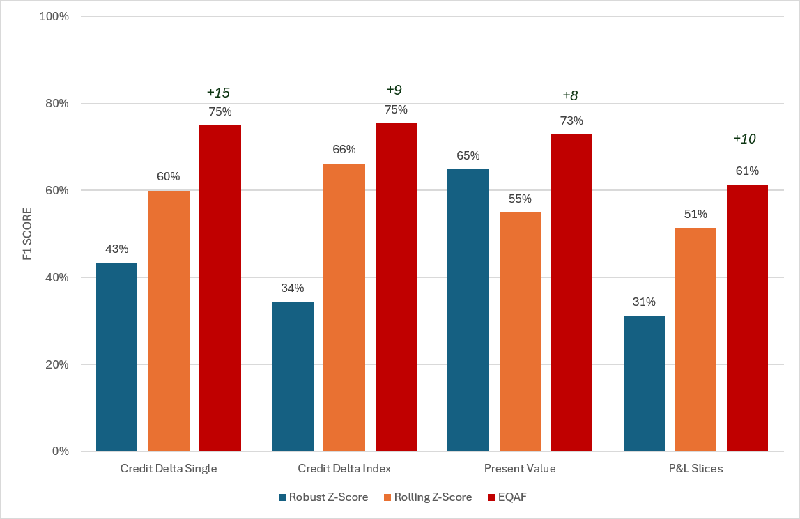

The EQAF employs a layered, unsupervised architecture that combines multiple outlier-detection methods, providing real-time monitoring of risk calculation integrity. By utilizing real data from 183 trades across 129 trading days, the framework demonstrates impressive efficacy, achieving F1-scores ranging from 61% to 79%. This is a marked improvement over individual methods, which typically fall short with scores of 6% to 66%.

The Science Behind It: Methodology

The methodology is unique in its design, incorporating a variety of detection techniques including Robust Z-Score, Empirical CDF scoring, Hampel Filter, and Isolation Forest, among others. This ensemble method enhances coverage by ensuring that distinct types of anomalies, particularly those that statistical methods often miss, are effectively captured. A notable feature is the deterministic stale-value filter, which accurately identifies "stale" data inputs that remain unchanged over time, a critical aspect often overlooked by conventional methods.

Results That Matter: Performance Metrics

Through rigorous testing, researchers have established that the EQAF not only excels in detecting various types of anomalies but also adapts well to different datasets. The framework consistently outperforms individual detection methods across multiple scenarios, showcasing its ability to mitigate operational risks effectively. Additionally, the framework's modular design allows for customization based on the unique characteristics of each trading dataset, ensuring flexibility and precision in its applications.

Implications for the Future

The findings from this research have profound implications for model risk management and regulatory frameworks. By demonstrating that automated quality control of risk-calculation outputs is feasible, EQAF aligns with evolving regulatory demands for transparent, robust monitoring systems. Furthermore, the incorporation of a deterministic stale-value filter is not optional but essential, as it addresses a critical blind spot in traditional statistical methods, ensuring that operational failures are detected before they propagate through financial systems.

As the financial landscape becomes increasingly intricate and regulated, the ability to preemptively identify and address anomalies will be crucial. EQAF stands as a transformative solution capable of enhancing not only the supervision of individual institutions but also safeguarding the overall financial ecosystem from systemic risks.