Understanding Financial Market Behavior: How Trends Predict Volatility and Correlation

Recent research by Sara A. Safari and Christof Schmidhuber aims to revolutionize how we understand and predict the behavior of financial markets. Their groundbreaking work meticulously examines how current market trends impact future volatility and correlations between various financial assets.

The Key Concepts

At the core of their research is the realization that financial markets behave differently based on the prevailing trend—whether prices are ascending or descending. The authors identified a clear pattern: during strong trends—particularly downward trends—volatility and correlations among assets tend to rise consistently. This insight enhances previous models that primarily focused on expected returns.

Unpacking Trend Strength

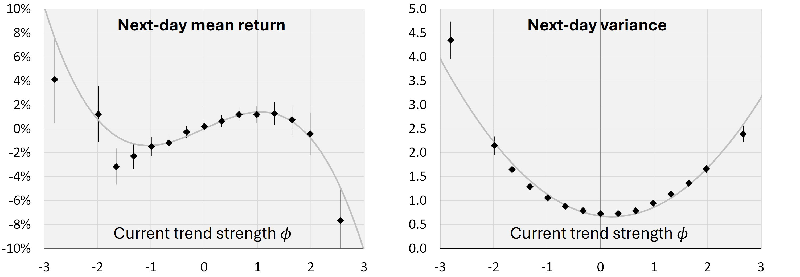

The researchers define 'trend strength' using statistical methodologies that aggregate daily market data over a wide range of assets and temporal scales. Essentially, they measure how strongly a market is trending towards gains or losses by analyzing the day's price movements compared to a historical average.

Using this method, they derived a model that predicts the next-day return based on today's trend strength. Their findings indicate that future volatility can be accurately predicted using a quadratic polynomial model based on the day’s trend—a refinement that makes predicting financial risks much more reliable.

Refining Market Models

The research also critiques existing mean-reversion models, suggesting that they neglect the influence of contemporary market trends. By integrating trend strength into these models, the authors propose a more dynamic forecasting mechanism for market behavior that grants investors an advanced tool for risk management—particularly useful during financial crises.

Practical Applications for Investors

What does this mean for everyday investors? For one, understanding trends could allow investors to better anticipate fluctuations in market volatility and adjust their portfolios accordingly. Enhanced predictive capabilities not only serve individual investors but can also guide institutional practices, potentially leading to more stable financial markets.

The Bigger Picture

The implications of Safari and Schmidhuber's research extend beyond mere prediction. By modeling financial markets analogously to critical phenomena in physics, the authors open the door to innovative ways of thinking about asset correlations and market stability. Their work suggests that financial markets operate in a complex landscape influenced by both internal and external pressures, requiring a nuanced approach to market modeling.

As financial markets continue to evolve, the ability to quantify and understand the intricate relationships between trends, volatilities, and correlations will be vital. This research not only contributes to the academic literature but also equips market participants with better tools and insights for navigating the ever-changing terrain of finance.

In summary, the exploration of trends in financial markets by Safari and Schmidhuber marks an important step forward. By enhancing our understanding of volatility and correlation dynamics, they are shaping the future of financial risk management and investment strategies.

Authors: {Sara A. Safari, Christof Schmidhuber}