Preventing Financial Disasters: The Breakthrough Ensemble Framework for Detecting Anomalies in Banking Risk Systems

In the high-stakes world of investment banking, the integrity of risk calculation systems is paramount. Errors in these systems can lead to catastrophic financial losses, as seen in infamous incidents like the London Whale and the Société Générale trading scandal. A groundbreaking paper titled "How to Spot Outliers: An Ensemble Anomaly Detection Framework" by Daniil Peysakhovich and Rafał Sieradzki addresses this critical issue by introducing the Ensemble Quality Assessment Framework (EQAF), a sophisticated tool designed to enhance the monitoring of risk calculation outputs in real-time.

The Need for Effective Anomaly Detection

Modern investment banks depend on complex systems to calculate risk metrics, which guide crucial decisions regarding capital allocation and risk management. However, when these systems fail, the consequences can ripple throughout the institution and even impact the wider financial system. Regulators are increasingly demanding robust monitoring to prevent such failures, yet current methodologies often fall short, particularly in detecting subtle anomalies.

The Innovation Behind EQAF

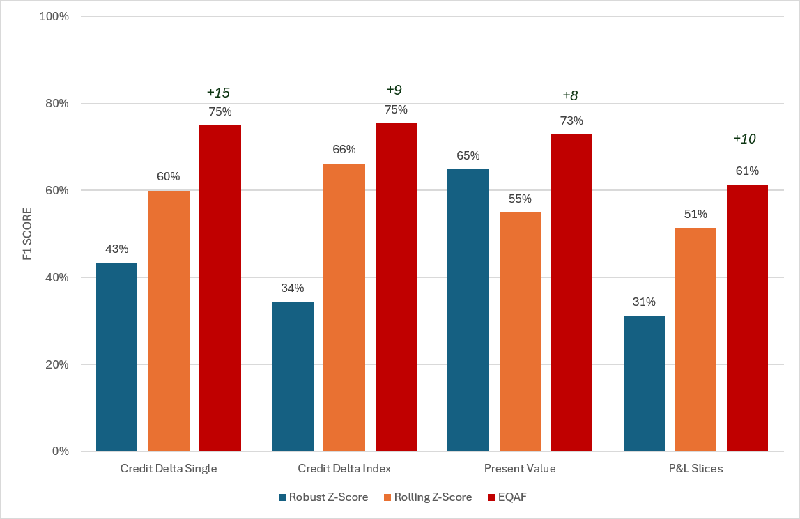

The EQAF provides a layered, unsupervised architecture that integrates various outlier detection methods to enhance the accuracy of anomaly detection. By utilizing a combination of statistical and machine-learning techniques, the framework successfully identifies abnormalities that individual methods might overlook. In their study, Peysakhovich and Sieradzki demonstrated that EQAF drastically improves detection rates, achieving F1-scores between 61% and 79%, a significant leap compared to traditional methods.

How EQAF Works

One of the standout features of EQAF is its ability to detect 'stale-value anomalies'—situations where risk outputs remain unchanged despite market movements, thereby masking significant risks. Traditional statistical methods are blind to these errors, as they appear statistically similar to normal observations. EQAF incorporates a deterministic filter specifically designed to catch such anomalies, raising the detection rate for stale values from 0% to 100%.

Empirical Success

The authors conducted experiments using real-world credit-derivatives data from UBS Investment Bank. Through a controlled anomaly injection protocol, they tested eight operationally realistic scenarios and established that EQAF significantly outperformed the best individual detection methods across multiple datasets. The framework is not just reactive; it enhances the proactive identification of risk issues before they escalate into financial disasters.

Implications for Financial Institutions

The findings from this research have profound implications for risk management in the banking sector. As regulatory demands evolve, financial institutions must integrate automated, scalable quality control like EQAF into their risk management frameworks. This could not only prevent financial losses but also bolster the overall stability of the financial system by catching errors before they propagate.

Implementing such innovative frameworks ensures that banks not only comply with evolving regulations but also protect themselves from potentially catastrophic financial consequences. The EQAF represents a significant step forward in the quest for a more resilient financial infrastructure.